Introduction

Turkey’s largely free-market economy is driven by its industry and, increasingly, service sectors, although its traditional agriculture sector still accounts for about 25% of employment. The automotive, petrochemical, and electronics industries have risen in importance and surpassed the traditional textiles and clothing sectors within Turkey’s export mix. However, the recent period of political stability and economic dynamism has given way to domestic uncertainty and security concerns, which are generating financial market volatility and weighing on Turkey’s economic outlook, According to the CIA World Factbook.

Current government policies emphasize populist spending measures, while the implementation of structural economic reforms has slowed. The government is playing a more active role in some strategic sectors and has used economic institutions and regulators to target political opponents, undermining private sector confidence in the judicial system. Between July 2016 and March 2017, three credit rating agencies downgraded Turkey’s sovereign credit ratings, citing concerns about the rule of law and the pace of economic reforms.

Turkey remains highly dependent on imported oil and gas but is pursuing energy relationships with a broader set of international partners and taking steps to increase the use of domestic energy sources, including renewables, nuclear, and coal. The joint Turkish-Azerbaijani Trans-Anatolian Natural Gas Pipeline is moving forward to increase the transport of Caspian gas to Turkey and Europe, and when completed, will help diversify Turkey’s sources of imported gas.

Gross Domestic Product

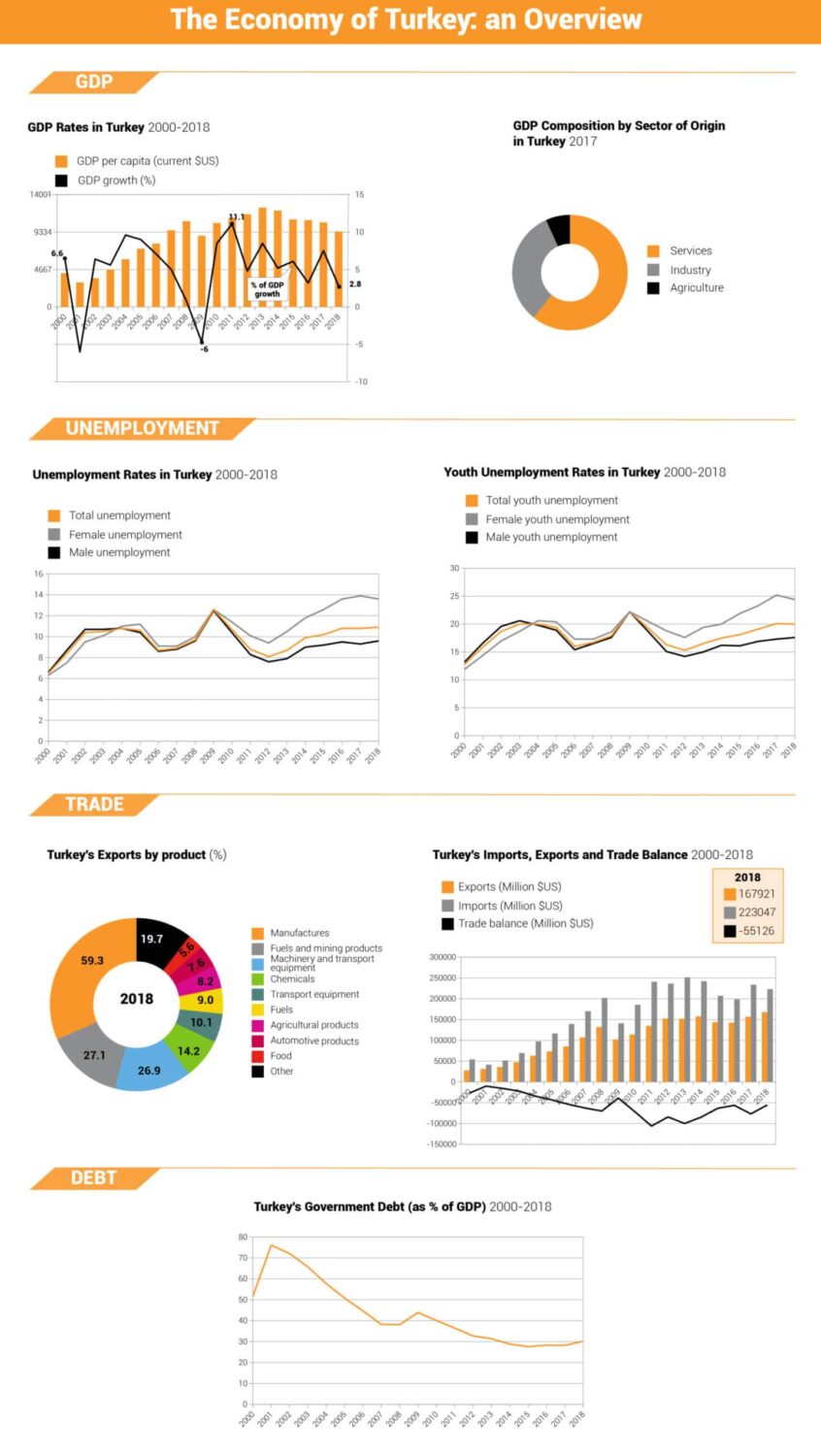

The growth rate of the Turkish economy had deteriorated significantly to 2.6 per cent by the end of 2018, compared to 7.4 per cent in 2017. According to data released by the Turkish Statistical Institute in March 2019, this was the result of a sharp contraction experienced during the previous quarter, which amounted to 3 per cent as a result of the decline in the value-added of the construction sector by 8.7 per cent, the industrial sector by 6.4 per cent, the agricultural sector by 0.5 per cent and the services sector by 0.3 per cent.

Gross domestic product (GDP) fell to $784.1 billion in 2018 from $851.5 billion in 2017. In the fourth quarter of 2018, GDP was $184.9 billion, which is the lowest amount since the first quarter of 2017 when it reached $175.9 billion, while per capita GDP at the current value was about $960,000 in 2018.

| Indicators | measuring unit | 2016 | 2017 | Change ± |

| GDP (at constant 2010) | Trillion US$ | 1.123 | 1.206 | 0.083 |

| GDP growth (annual) | % | 3.2 | 7.4 | 4.2 |

| GDP per capita (constant 2010) | US$ | 14,117 | 14,936 | 819 |

| GDP (at current value) | Billion US$ | 863.722 | 851.549 | -12.173 |

Source: World Bank.

International Market Position

Turkey was ranked 53rd out of 137 countries covered by the Global Competitiveness Index 2017-2018, two places lower than 2016-2017 but still higher than the historic low of 43rd place in 2012. In the year 2017/2018, the strongest enhancements to the latest technology as well as mobile broadband subscriptions are expected to increase from 51 per cent of the population in 2015 to 67 per cent of the population in 2016. To move forward, Turkey must improve its institutional framework, continue to remove the strict rules in its labour markets, and enhance the efficiency and stability of its financial markets. The devaluation of the lira in 2017 helped Turkish exports, and the government stimulated domestic demand by strengthening monetary and fiscal policies.

Infrastructure

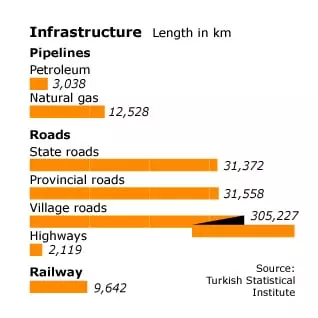

During the Hamidian period (1876-1909) and the Kemalist period (1922-1945), Turkey focused on the construction of railways, 10,900 kilometres in length, ranking the country 23rd in the world in this field. Since the 1950s, however, Turkey has neglected railways in favour of roads and highways – 65,049 kilometres of roads in 2012, of which 2,119 kilometres was highways, 31,372 kilometres trunk roads, and 31,558 kilometres secondary roads.

In 1990-2000, many new airports were constructed; there were 99 active airports in 2010.

Investments in the road and air sectors will continue in the coming decades, but, according to the Ministry of Transport, it appears that the Erdoğan government wishes to rebalance its policy in the infrastructure sector and construct at least 10,000 kilometres of high-speed railways, with the help especially of Chinese companies. Double-track railways between Ankara and Istanbul and between Ankara and Konya are currently under construction.

Of great importance in the infrastructure sector, Istanbul has become an ‘infinite city,’ where not even the construction of a third bridge connecting Europe and Asia will solve the complex traffic problem. The underwater metro project between the European and Anatolian coasts, which is currently under construction, will probably not relieve the traffic congestion between the two continents.

A maritime country par excellence, Turkey has many ports, on the Black Sea (Rize, Trabzon, Giresun, Ordu, Samsun, Zonguldak) and on the Mediterranean (Dörtyol, Iskenderun), as well as Istanbul (on the Bosporus) and Izmir (on the Aegean). These are all relatively low-capacity ports, compared to those of Europe.

Energy

For an in-depth overview of Turkey’s energy sector click on the button below.

Industry

Turkish industry employs 19.9 percent of the labour force; its major industries are steel/metallurgy, textile and clothing, petroleum products, food, and automotive. Although the Istanbul-Kocaeli/İzmit basin, the Çukurova plain (with Adana as its regional capital), and the Izmir region are still considered the three traditional industrial areas, many other regions, from Kayseri to Gaziantep, and from Adıyaman to Denizli, have emerged in the last twenty years as centres of industrial production.

Construction

Rapid urbanization during the last decades and regional developments from 1980 to 1990 (e.g., the Iraq-Iran War and the collapse of the Soviet Union) enabled the construction sector in Turkey to develop externally and become important on the international stage. Ankara, at the center of Turkey’s highway and railway networks, demonstrates how the construction sector has also benefited greatly from infrastructure development and constructed large cities.

The construction sector, which employs 6.33 percent of the labour force, has also benefited from the construction of airport facilities in Turkey and its neighbourhood, including in Arbil/Hewler, in Iraqi Kurdistan.

Earthquakes in the Marmara region (İzmit, 1999) and in Van (2011) have revealed the extent of corruption in the construction sector, the lust for money, and the lack of effective and genuine government supervision, as well as the poor quality of construction. In Istanbul, in particular, most of the buildings that were destroyed by the earthquake (which killed nearly 20,000 people) were home to lower-middle-class people who had invested their life savings in those newly constructed buildings.

Trade and Banking

The density of commercial and financial networks in Turkey is explained, in part, by the spread of hypermarkets since the 1980s, the government’s facilitation of the creation of local banks or branches of foreign financial institutions, and the multiplication of industrial production centres. It is estimated that about 150 American-style shopping malls will have been constructed in Istanbul in the late 2010s. This dynamism has made the ‘tertiary sector’, which employs almost half of the labour force, the leading sector in the country.

Turkey has 48 banks, including 31 retail banks (3 public, 11 private, and 16 foreign), 13 development and investment banks, and 4 participatory-cooperative banks. These banks have more than 9,712 branches and 181,588 employees. The largest banks are Ziraat Bankası (Agricultural Bank), İş Bankası (Labour Bank), Akbank, and Garanti Bank.

Turkey, which is considered an emerging economy and was in the midst of economic transformations, was relatively unaffected by the 2008-2012 financial crisis.

The strength of domestic consumption and the radical restructuring of the banking sector after the 2000-2001 crisis helped make Turkey somewhat resistant to the global shock, but many economists consider the lull a warning of upcoming storms in the Turkish economy.

Between 2005 and 2010, the foreign-trade deficit increased from 5 to 10 percent of GDP, and growth was maintained by easy consumer access to credit cards, a form of consumption that may lead to a crisis similar to that in the subprime-mortgage business. The Bank Association of Turkey reported that the number of credit-card users increased from 3,735,000 to 5,136,100 from 2007 to 2011 and that credit-card consumption, which represented 16.5 percent of the GDP in 2007, increased to 22 percent over the next five years. Consumer debt amounted to USD 95 billion in May 2012.

Tourism

The income generated by the tourism sector is expected to reach USD 10 billion in 2012. Domestic tourism is booming in Turkey, but most tourists are foreign. The number of foreign tourists increased from fewer than 10 million in 1998 to 31 million in 2011, generating a net profit of USD 23 billion over that period. This increase can be explained by factors both long-term (an influx of tourists from Russia, Turkey’s attractions, and the low prices) and short-term (instability in Arab countries in 2011-2012).

Informal Sector

Research on the informal sector in Turkey is contradictory and unreliable, but several factors suggest that it plays a major role in the economy of the country. Family structures remain strong, which leads to the unpaid labour of women and children. The ties of hemșehrilik (solidarity between people from the same city or region, who often congregate in the same neighbourhood in their new place of residence) remain strong and contribute to the structuring of the economic world at a micro level.

Similarly, although rapid urbanization is now under control, it created, in recent decades, areas largely beyond the control of the state. Finally, Maffia-like economic structures are extremely powerful in some fields, such as cross-border trade and sectors in which subcontracting is important.

Given all these factors, economist Osman Altuğ estimated that, at the beginning of the 1990s, one-third of the labour force (around 5 million people) worked in the informal sector, with revenues sometimes exceeding 50 percent of GNP. The TİSK (Turkish Confederation of Employers’ Unions) estimated that 1,700,000 people worked in the informal sector at the beginning of the 2000s.

Regional Development

Regional inequalities have always been large in Turkey: Istanbul and its neighbouring cities, especially Kocaeli (İzmit), take the lion’s share of private and public investment. These two cities, with a total population of 14,815,816, are responsible for 26.2 percent of the GDP. The contribution to the GDP of Diyarbakır, a city the same size as Kocaeli (1,518,958), is 1.1 percent.

The contribution to GDP of cities such as Bitlis (population 228,767) and Muş and Şırnak (population more than 400,000 each) does not exceed 0.1 percent. The peripheral situation of these cities cannot alone explain the causes of poverty: under the Kemalist Republic, authorities refused to invest in sectors other than military and security.

The State Planning Organization (Devlet Planlama Teșkilatı) has attempted since the 1960s to address these inequalities.

With the creation of ‘large municipalities’ and new urban entities, followed by the establishment of Regional Development Agencies (Bölgesel Kalkınma Ajansları) in the 2000s, the state produced a new development policy that benefited the regions and provinces, but the results were occasionally disappointing.

The cases of Diyarbakır and Urfa show how measures remain unimplemented due to the lack of necessary human, financial, and technical resources. The results were mixed: the per capita income in some Kurdish provinces, for instance, is one-tenth that of large cities in western Turkey.

While the Central Anatolia region benefits from its proximity to the Aegean and Mediterranean regions and the emergence of new industrial centres, the coasts of the Black Sea, with the exception of some areas such as Trabzon, are still neglected.

Work and Migration

The labour force in Turkey totals 46.9 million, of which 24.5 million are women. (Official sources estimate the participation of women in work at only 26 percent.) 3.5 million are unemployed, and 500,000 young people enter the job market every year. A study prepared by Koç University, in Istanbul, shows the difficulties faced by young people in finding their first job, particularly in an urban context.

According to another report prepared by the pro-government think tank SETA, agriculture’s share of the job market decreased from 36 percent (7.7 million) in 2000 to 24 percent (5.2 million) in 2009. Fifty-three percent of those between 20 and 24 were able to find jobs in rural areas, compared to 35 percent in urban areas.

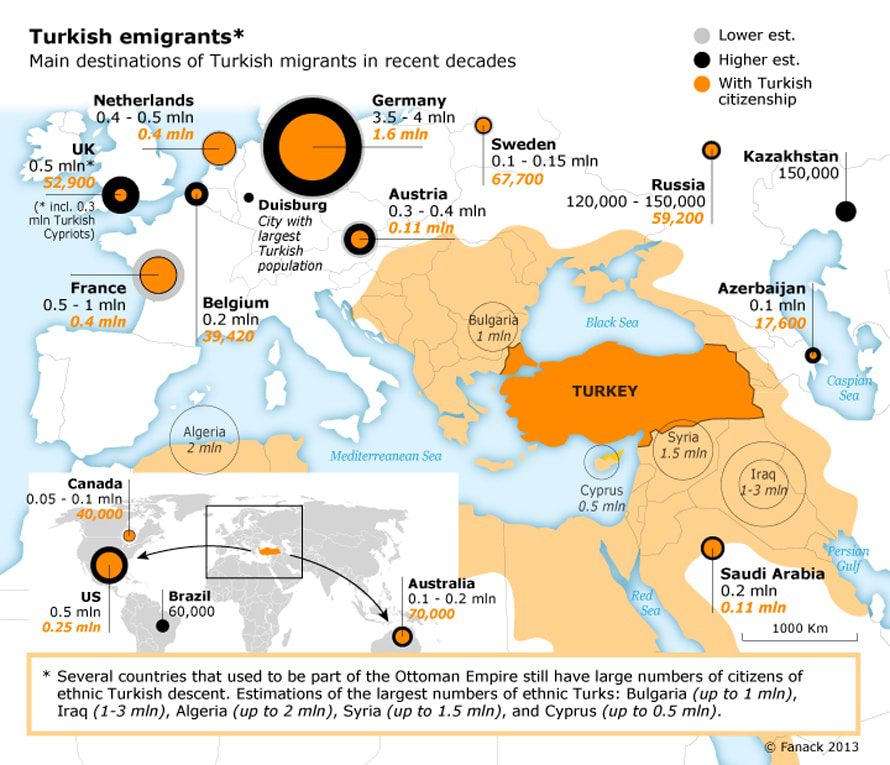

The emigration of labour has long been an issue in Turkey, but emigration has been stabilized today and even reversed. It is estimated that the number of Turkish nationals and their descendants in Europe, the US, and Australia total 4 million, or more than 5 percent of Turkey’s population.

According to the deputy chairman of the Turkish-German Chamber of Commerce and Industry, many highly qualified third-generation Turkish immigrant professionals are returning to Turkey from Germany to pursue an occupation, marginally reversing the migration to Europe that began in the 1960s.

Even if the rush to the western El Dorado is fading, internal migration continues. According to the above-mentioned SETA report, Istanbul, Eastern Marmara, and the Aegean region are home to nearly 68 percent of wage earners, which explains the continued migration of labour from the rest of Anatolia to these locations.

Furthermore, the war and massive destruction in the rural areas in Kurdistan in the 1990s also strengthened internal migration, leading to the formation of large Kurdish communities in Istanbul, Ankara, Izmir, Adana, Mersin, and many other cities.

Turkey has become a transit hub for Afghani and Iraqi immigrants and sometimes African immigrants bound for Europe. The number of these immigrants is estimated at hundreds of thousands; they are often employed in the informal sector, pending possible departure for Europe. These immigrants represent 2 percent of the Turkish labour force or nearly one million people. It is estimated that Turkey has about 80,000 Armenian immigrants without legal status.

Poverty

Between 2004 and 2016, the poverty rate in Turkey dropped significantly from 27.3 per cent to 9.9 per cent, measured using the poverty line in upper-middle-income countries of $5.50 per person per day (2011 purchasing power parity). Income and employment growth were key factors in reducing poverty during that period, despite the sharp economic downturn of 2008-2009. In contrast, unemployment has risen since 2018. Overall inflation rose to 20.3 per cent in January 2019, while food price inflation rose to 30.9 per cent. The poor are disproportionately affected by food price inflation because they spend a larger share of their income on food.

In response, the government increased the minimum wage by 26 per cent in January 2019 and announced employment support programmes to protect low-income families. In a state of extreme uncertainty, the World Bank forecast a 1 per cent economic growth rate for 2019 with a moderate recovery in 2020-2021. It also projected that poverty levels would reach 9 per cent between 2018 and 2020 and that the number of poor would rise.

Inequality has increased over the last decade. Although the Gini index fell from 42.2 in 2003 to 39.0 before the economic crisis in 2008, it increased to 41.9 in 2016. The increase in inequality resulted from the impact of the economic crisis on labor market returns.

Average per capita consumption growth in the lowest level rose by an average of 40 per cent which is still below the higher percentage recorded between 2011 and 2016 (60 per cent). The common prosperity over the same period was negative at -0.94 per cent.

Latest Articles

Below are the latest articles by acclaimed journalists and academics concerning the topic ‘Economy’ and ‘Turkey’. These articles are posted in this country file or elsewhere on our website: