Contents

Introduction

In 2017, the economic outlook in the West Bank – the larger of the two areas comprising the Palestinian Territories – remained fragile, as security concerns and political friction slowed economic growth. Unemployment in the West Bank remained high at 19.0% in the third quarter of 2017, only slightly better than 19.6% at the same point the previous year, while the labor force participation rate remained flat, year-on-year.

Longstanding Israeli restrictions on imports, exports, and movement of goods and people continue to disrupt labor and trade flows and the territory’s industrial capacity, and constrain private sector development. The PA’s budget benefited from an effort to improve tax collection, coupled with lower spending in 2017, but the PA for the foreseeable future will continue to rely heavily on donor aid for its budgetary needs and infrastructure development.

Movement and access restrictions, violent attacks, and the slow pace of post-conflict reconstruction continue to degrade economic conditions in the Gaza Strip, the smaller of the two areas comprising the Palestinian territories. Israeli controls became more restrictive after HAMAS seized control of the territory in June 2007. Under Hamas control, Gaza has suffered from rising unemployment, elevated poverty rates, and a sharp contraction of the private sector, which had relied primarily on export markets.

Since April 2017, the Palestinian Authority has reduced payments for electricity supplied to Gaza and cut salaries for its employees there, exacerbating poor economic conditions. Since 2014, Egypt’s crackdown on the Gaza Strip’s extensive tunnel-based smuggling network has exacerbated fuel, construction material, and consumer goods shortages in the territory. Donor support for reconstruction following the 51-day conflict in 2014 between Israel and HAMAS and other Gaza-based militant groups has fallen short of post-conflict needs.

Gross domestic product

The real gross domestic product (GDP) growth rate of the Palestinian economy (West Bank and Gaza Strip) reached 2 per cent in the first half of 2018, a number that masks a severe deterioration in Gaza.

In recent years, Gaza’s economy has been kept afloat by remittances, including donor assistance, and expenditures through the Palestinian Authority’s budget that accounted for 70-80 per cent of Gaza’s GDP, according to the World Bank.

However, remittances from these two sources have recently declined sharply, leading to a 6 per cent contraction of economic activity in Gaza in the first quarter of 2018.

In contrast, the economic growth rate in the West Bank was 5 per cent during the same period, mainly due to public consumption. On the demand side, growth was concentrated in wholesale, retail and construction, as these activities were least affected by Israel’s imposed restrictions system.

In the context of this scenario, which presupposes Israel’s continued restrictions system and the continued internal division between the West Bank and Gaza Strip, private sector activity is not expected to recover. The World Bank anticipates that real GDP will grow between 0.5 per cent and 1.6 per cent between 2019 and 2021.

This level of growth predicts an annual decline in per capita real income between 2-3 per cent. Inflation will remain under control, with an average of around 2 per cent between 2019-2021.

| Indicators | measuring unit | 2016 | 2017 | Change ± |

| GDP (at constant 2010) | Billion US$ | 11.767 | 12.137 | 0.369 |

| GDP growth (annual) | % | 4.7 | 3.1 | -1.6 |

| GDP per capita (constant 2010) | US$ | 2.655 | 2.494 | -161 |

| GDP (at current value) | Billion US$ | 13.426 | 14.498 | 1.062 |

Source: World Bank.

Poverty

The poverty rate in Palestine, measured using the national poverty line, increased from 25.8 per cent to 29.2 per cent between 2011 and 2016/2017.

However, the situation in the West Bank and Gaza diverged sharply.

The West Bank experienced a slight improvement, where the proportion of the population living below the poverty line declined from 17.8 per cent to 13.9 per cent. In contrast, poverty in Gaza increased from 38.8 per cent to 53 per cent.

Poverty rates, using the international poverty line of $5.50 per person per day (2011 purchasing power parity) in upper-middle-income countries, are close to the national average. Living standards in both territories remained fragile.

| Indicators | Number of Poor (thousand) in 2016 | Rate (%) in 2016 |

| National Poverty Line | 1,329.1 | 29.2 |

| International Poverty Line 5.2 in Israeli new shekel (2016) or US$1.90 (2011 PPP) per day per capita | 43.5 | 1.0 |

| Lower Middle Income Class Poverty Line 8.7 in Israeli new shekel (2016) or US$3.20 (2011 PPP) per day per capita | 226.1 | 5.0 |

| Upper Middle Income Class Poverty Line 15 in Israeli new shekel (2016) or US$5.50 (2011 PPP) per day per capita | 1,072.3 | 23.6 |

Source: The World Bank.

In the West Bank, poverty is susceptible even to small spending shocks: a 5 per cent change in spending could increase national poverty by as much as 16 per cent, while a 15 per cent change could increase poverty by 50 per cent. In Gaza, more than 75 per cent of households depended on some form of social assistance in 2017.

Consumption growth in the West Bank was pro-poor, benefitting the poorest 40 per cent more than the average, while the cost of economic desperation in Gaza and refugee camps was slightly more borne by the lower economic levels of the population. Accordingly, inequality decreased significantly in the West Bank but increased slightly in Gaza.

Despite low employment in 2011-2017, changes in labour market earnings were the main driver of the decline in poverty and inequality in the West Bank. In particular, the consistent increase in the share of paid jobs reduced poverty and inequality. In contrast, the decline in remittances was behind most of the increase in poverty in Gaza, outweighing the positive contribution of labour earnings during this period.

Agricultural Sector

Agriculture is one of the most important and oldest sectors of the Palestinian economy, as many crops are produced to fulfil the needs of the population and achieve food security and economic growth. Statistics indicate a significant drop in the percentage contribution of the agricultural sector to GDP, from 37% in the mid-1970s to 13.4% in 1994, 6.5% in 1999, and 5.6% in 2012.

The percentage value added to GDP by agricultural activity dropped to 3.9% at the end of 2014, although preliminary estimates by the PCBS predicted a slight increase of 4.1% at the end of 2015, based on optimistic economic-growth expectations.

Agriculture covers about 1.854 million acres or 31% of the total area of the West Bank and the Gaza Strip, 91% of which is in the West Bank and 9% in the Gaza Strip. Some 62.9% of the agricultural land is located in Area C, which is under Israel’s administrative and security control.

The agricultural sector’s role is not limited to economic and social aspects; it is also a key player in protecting the land from confiscation and settlement activities and guaranteeing the protection and the legal right to the use of water. The agricultural sector is also a major source of jobs, accounting for about 15.2% of the workforce, with a large percentage of workers, especially females, working in this sector unofficially.

The agricultural sector in Palestine faces many problems and obstacles, including those caused by the Israeli occupation and related to natural resources and administrative laws. Obstacles related to Israeli practices include the construction of the Separation Wall and the resulting isolation and confiscation of land in order to build settlements, the conversion of large areas of Palestinian land into nature reserves and areas used as Israeli military training grounds, the construction of bypass roads, the destruction of Palestinian water wells in agricultural areas, and the reduction of the Palestinian share of water.

Other practices include curbs on the freedom to export crops and import raw materials, and the prohibition of fishing further than six nautical miles off the Gaza Strip coast, out of the 20 nautical miles provided in the Paris Protocol.

Other challenges related to natural and environmental resources include limited water resources and agricultural land, improper use of chemicals, the lack of revenue from agriculture, and the high risk of crops being burnt by settlers, which has led many people to hesitate to work in that sector, given the absence of an agricultural insurance system that compensates farmers.

A study prepared by the Palestine Economic Policy Research Institute (MAS) in Ramallah concluded that Palestinian farmers face legal, administrative, and technical issues, including agricultural land registration, high prices of agricultural land, urban expansion, and the distribution of land to heirs because such small plots of agricultural land are economically unworkable. This overview shows the magnitude of the suffering of Palestinian farmers in their effort to survive, especially considering that land is at the core of the Israeli-Palestinian conflict.

Industrial Sector

The industrial sector—including the extractive, processing, and handicrafts branches—is the second most important sector. It contributes 13.1% to the GDP, amounting to nearly one billion dollars (see chart above), and it comes second after the services sector in GDP.

The extractive industry that involves the use of quarries for cutting marble and other stones mainly in the cities of Nablus, Ramallah, and Hebron. The mountains of Palestine contain limestone and layers of other, varicoloured stone, which are exported to several countries around the world.

Statistics show that the marble and other stone industries contribute 12% to the total industrial output of Palestine. Also, minerals such as phosphates, asphalt, and mud are extracted from the western shores of the Dead Sea; glass sand is extracted in Hebron, Ramallah, and Nablus; and Sulphur is extracted in the Gaza Strip.

Handicrafts are the largest industrial sector and include trades such as textiles, footwear, ceramics, pottery, olive wood, seashells, coloured glass, soap, leather tanning, embroidery, and manufacturing bamboo products.

The food and agricultural industry is the largest and most important processing industrial sector related to processing. It includes the production of confectionery, dairy products, processed meats, beverages, pasta, cereals, canned food, oils, and animal feed. The food sector constitutes about 24% of the total industrial sector, amounting to about 400 million US dollars and employs about 16.8% of the total Palestinian workforce.

The PNA developed a strategy for manufacturing and industrial development in order to achieve a range of goals, including equitable growth and balance between the agricultural and industrial sectors, and between satisfying domestic demand and encouraging the export of goods. As a result infrastructure, including a transportation network, has been developed, and industrial zones have been established in most Palestinian cities, including Jericho, Jenin, Ramallah, Nablus, Bethlehem, Hebron, and Gaza, among others. In order to create a healthy investment environment in Palestine, a legal system has been established to attract Palestinian expatriates and foreign investors by providing tariff and tax exemptions for new investors for up to five years, under the Investment Promotion Law.

Like the agricultural sector, the industrial sector suffers from a wide variety of challenges, including the Israeli obstacles mentioned above. The competitiveness of Palestinian industries is modest, compared to regional and international markets, and heritage-focused handicraft industries prosper only where tourism is active in Palestinian areas; the lack of stability caused by the volatile political situation has affected the situation for more than a decade.

Services Sector

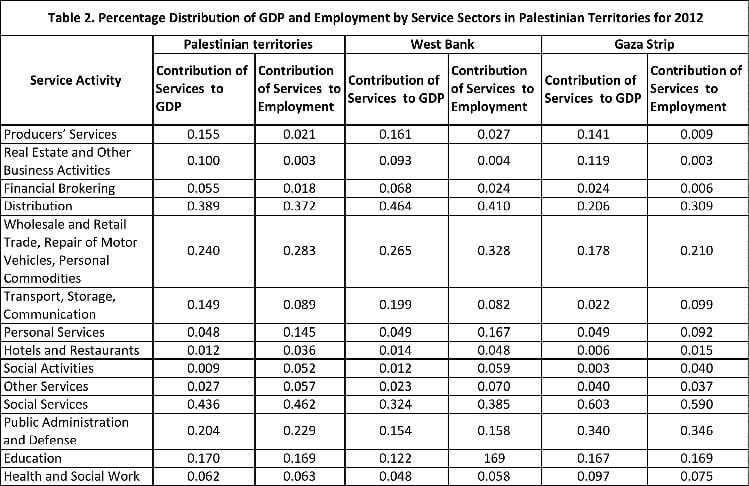

The Palestinian services sector has grown substantially recently, contributing greatly to the Palestinian economy. The percentage value added to GDP by services and other items for the year 2014 amounted to 63.1%, (see the table above), about 57% in 2012, and about 52.2% in 2000. The services sector employed about 62% of the total Palestinian workforce. The sector covers all real-estate activities, banking, telecommunications, insurance, transportation and distribution services, and hotels and restaurants, among others.

Construction Sector

The construction sector constitutes one of the key Palestinian economic activities, in terms of contribution to GDP and employment and in term of its direct impact on many other economic activities. Most economic reports indicate a significant growth in the construction and real-estate investment sectors in Palestine. This clearly shows in the construction of new residential suburbs around several Palestinian cities. This is not surprising, as the construction sector in the field of infrastructure and housing has been growing since the establishment of the PNA, which has sought to create a solid infrastructure for a future Palestinian state and provide sufficient housing for its citizens.

The Palestinian Investment Fund and some banks operating in the Palestinian territories provide financing to Palestinian citizens to enable them to own their own houses and repay their loans in monthly instalments.

Data published by the PCBS indicate that the housing sector remains one of the most important resources for development in Palestine, with the ratio of investment in housing to GDP since the establishment of the PNA amounting to about 21% in 1994, and 26% in 1999.

This percentage did, however, drop significantly after the outbreak of the Second Intifada in 2000, to about 16.6% and continued to decline in subsequent years, to 13.8% at the end of 2007. The percentage did rise to 15.4% at the end of 2013.

The construction sector also contributes to Palestinian employment, increasing the number of workers from 34,600 in 1993 to 88,300 at the end of 1998. Since the establishment of the PNA, which began to build its institutions and rehabilitate Palestinian infrastructure, employment in the housing and construction sectors has increased by several times.

However, employment dropped significantly during the years of the Second Intifada, although there was a noticeable improvement in employment in housing construction during the relative calm from 2003 to 2005.

Data presented by the PCBS showed a rise in spending on the construction of new buildings in 2013 to about 913 million US dollars (711.5 million in the West Bank and 201.6 in the Gaza Strip). Moreover, the value of spending on maintenance and capital improvements to existing buildings rose slightly over the previous year, amounting to more than 650 million US dollars.

The significant rise in the construction sector in Palestine, especially in the Gaza Strip, is due to the destruction wrought by Israel during past wars. Media reports show that the Israeli attacks on the Gaza Strip between 2008 and 2014 resulted in the complete destruction of more than 10,000 residential and service buildings and that more than 34,000 other buildings were seriously damaged.

Residential buildings and industrial and agricultural facilities were not the only targets of Israeli attacks. Infrastructure, including road networks, wastewater and water-supply systems, electricity distribution networks, power stations, and bridges were targeted during the three wars. The Gaza Airport was destroyed in 2002, and Israel did not allow it to be rebuilt.

The conference on the reconstruction of the Gaza Strip held in Cairo on 12 October 2014 pledged to provide financial assistance to the Strip amounting to 5.4 billion US dollars. Construction is largely dependent on the supply of construction materials, particularly cement and steel, deliveries of which into the Gaza Strip have been delayed by Israel.

The delay in the reconstruction of the Gaza Strip has many causes, including the Israeli siege and the mechanism established by UN Envoy Robert Serry to monitor the influx of construction materials, a mechanism that will fail: statistics show that the UN proposal would require more than ten years for the reconstruction of the Gaza Strip.

Unemployment

In all countries of the world, unemployment is considered a ticking bomb that threatens both economic and social stability. The PCBS reported that unemployment in the West Bank and the Gaza Strip stood at about 27% by the end of 2014. The PCBS report noted that the number of unemployed reached 338,000 in 2014, a rate of 24% for males and 38% for females.

The number of unemployed individuals in the West Bank reached 143,000 (18% of the labor force) and 195,000 in the Gaza Strip (about 44% of the labor force).

The labor force in Palestine amounted to approximately 618,000 by the end of 2014, of whom 331,000 are employed in the West Bank, 188,000 in the Gaza Strip, 78,000 in Israeli territory, and 21,000 in Jewish settlements, the latter comprising mostly farmers working in the agricultural sector. The public sector has employed themost workers in the Gaza Strip, at 55%, compared to 45% of wage employees working in the private sector.

In the Gaza Strip, unemployment before the Israeli attacks on Gaza in July 2014 increased at an unprecedented rate. According to the PCBS data for the second quarter of 2014, the unemployment rate in the Strip reached 45% and the number of unemployed workers exceeded 200,000; these workers are responsible for more than 700,000 family members, or more than one-third of the population of the Gaza Strip. As a result, the poverty rate in the Strip rose to more than 50% by the end of 2014.

Because of the continued siege and the faulty reconstruction plan, economic conditions continued to deteriorate, and the unemployment rate rose again to 55%, with the total number of unemployed rising to 230,000 and 65% of the population living in the most extreme poverty conditions. Consequently, the number of recipients of UNRWA food assistance rose to nearly a million, or 60% of the total population of the Gaza Strip.

One important reason for the rising unemployment and poverty rates in the Gaza Strip is the crisis in the salaries of government employees. After the formation of the national unity government and the resignation of the “de facto government” in Gaza, the Palestinian government, led by Rami Hamdallah, did not recognise government employees hired in recent years in Gaza and refused to pay their salaries.

Therefore, more than 40,000 employees in Gaza have been receiving only 50% of their salaries since June 2014. This has caused recession and weakened purchasing power in the Gaza Strip, as unemployment and poverty rates increased enormously, causing further deterioration that may bring about the collapse of the entire economic system in the Strip.